It’s great to see canola prices soar.

Or rather, it’s great to see canola prices soar if you have canola and if you haven’t already priced it all at lower prices.

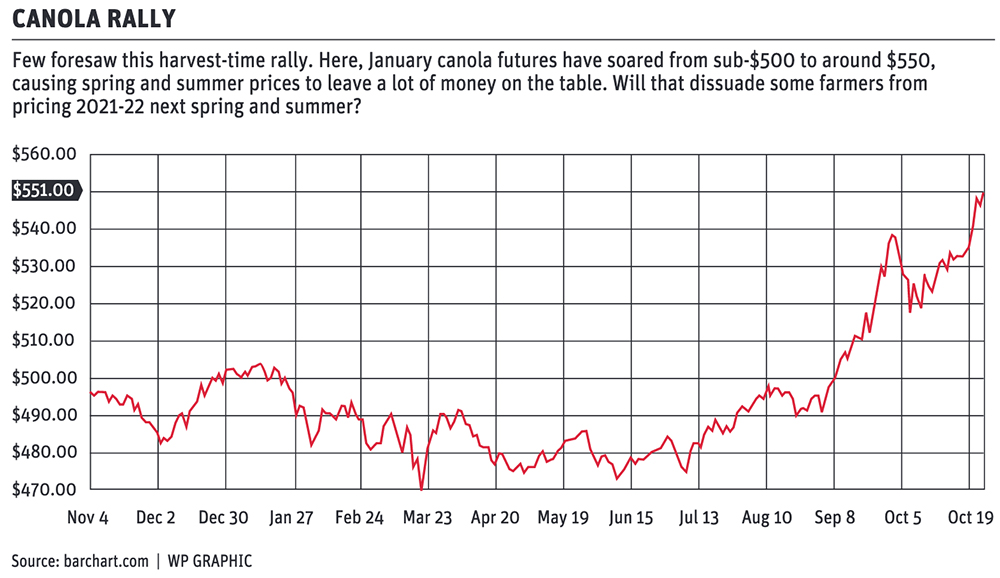

The counter-seasonal rally is certainly an epic aberration from normal patterns to watch, and for those with unpriced canola, it’s an early Christmas present. It’s also fascinating to watch for all sorts of industry and academic reasons.

But I wonder what the impact will be for diligent farm marketers. If farmers hedged this spring and summer, they did so at sub-$500 prices. That’s a lot of money to leave on the table.

Read Also

Agriculture needs to prepare for government spending cuts

As government makes necessary cuts to spending, what can be reduced or restructured in the budgets for agriculture?

Will this dissuade some farmers from hedging next year? That’s a risk when a hedge seems to have “lost” money.

In terms of the philosophy of hedging, nothing has been lost. The hedge, if properly constructed and executed, eliminates risk. It stops the price mattering.

Still, we’re all given to thinking about what could have been and this kind of a rally is the stuff of which farmers dream.

There are ways to avoid leaving money on the table from selling or pricing early. The crop can be marketed and then replaced on paper with call options. If they’re far enough out of the money, the premiums should be affordable, as they were this summer when few expected anything like this rally.

“We didn’t see it coming,” acknowledged Errol Anderson of ProMarket in Calgary, who had only a few clients who were willing to buy out-of-the-money canola calls this summer.

“We thought it was just wasted money, but here goes.”

Those call positions are now worth a bunch. If $510 January calls were selling for a $6 premium when futures were at $490, those positions are now worth $30-plus with futures around $550.

It’s a hard strategy to follow when prices are weak, because paying a premium effectively lowers the value of the canola hedged. But it paid off in this rally and didn’t lock people into anything beyond the premium.

It’s a strategy that might help prevent hedgers from abandoning their risk management program whenever they end up wrong-sided by an unexpected rally, like today’s. It can be a way to hedge against the psychology of having “left money on the table.”

Some farmers have no problem pricing diligently, following a program, and forgetting about what could have been. I chatted with some farmers on Twitter about this and they have the psychological strength to stick with a rational program even when it occasionally seems to have locked them out of potential big gains.

Others, I suspect, will have a tougher time handling the situation.

“The game of volatility is a psychological game,” noted volatility specialist Kris Sidial of the Ambrus Group on the Odd Lots podcast recently.

He was talking about the recent mania of amateurs for options trading, and about how risk management often gets killed by periods of complacency. People want to hedge when it’s too late to do much good, and they avoid hedging when it is theoretically but not psychologically most attractive.

“There will come a point in time when the market is just going up and people are going to be like, ‘I don’t need to place a hedge. Why do this? It’s taking away three percent yield from me per year. I don’t need this anymore.’ That’s when you will have more of these (episodes of sudden loss-making volatility) take place,” said Sidial.

A harvest time rally is a great thing for growers, at least in the short term. But it could be damaging if it causes farmers to give up on hedging in the future.

It’d be better to figure out what kind of a hedging strategy could remove some of that regret than to give up on hedging.

By the way, are you hedging today’s higher prices for old and new crop? Plus-$510 futures are available right into late 2022. That money’s sitting right on the table.