So here’s a healthy reality check for the uberbullish who see no end to the upside of ag commodity sales to China:

Barclays Commodity Research, in an analysis piece last week, labels ag commodities the “big losers” in China’s shifting demand for commodities.

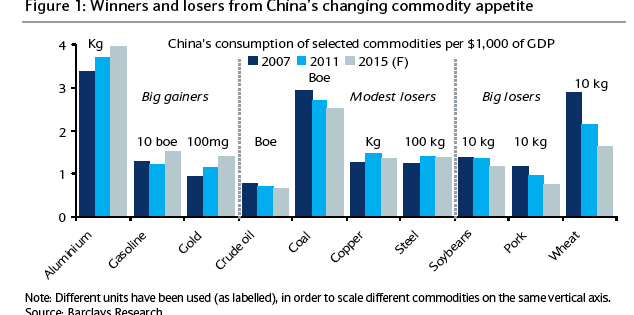

Here’s the chart the British investment bank carried on the front of the report entitled “The Dragon’s Appetite is Changing.”

Read Also

High prices see cow-calf producers rushing to incorporate

Farm accountants are reporting a steady stream of cow-calf producers rushing to get their operations incorporated ahead of selling their calves this fall.

Note that this doesn’t mean China won’t keep buying our oilseeds (canola rather than the soybeans in the graphic), pork or wheat. This looks at consumption related to GDP, so with China’s GDP growing steadily, if more slowly now, there’s every reason to believe that China’s consumption of what prairie farmers produce will continue well into the future. However, with growth rates of consumption of the ags slowing on a per capita basis, and actually falling in some ways, the outlook isn’t as blindingly light as China bulls like to have it.

It’s a worthwhile slap-in-the-face to those who are mega-bullish now on commodities forever. I’ve been a long time follower of the theories about and analysis of the long term commodity bull market – which we’re still in the middle of – and as with every bull market, the analysts who come in late tend to be most bullish and they help lead every sad sack into the last couple of legs of the rally. I go to so many conferences now where it is de rigueur to note that the world needs to double food production by some time or other, that the world is running out of fresh water, that folks in places like China are getting richer and want more meat, etc. etc. etc. In other words, there’s never an end to this bull market for farmers. That’s the implication.

To me, that’s crap thinking, because connecting farm profits to steadily growing demand is often undermined by two things: booming productivity gains and ebbs and flows of demand. Malthusian thinking sees no way that the farmers of the world can keep up with increasing demand, therefore profitability will be endless. Finite land base plus spiralling world population equals a tighter and tighter food supply. If you’ve got the land, you can’t help but make the money. But our busy scientists and profit-hungry companies have been finding ways of boosting crop yields at an incredible pace – just look at canola and corn over the past 20 years – and our vets and breeders have found ways to produce a heck of a lot more piglets per sow in recent years. So we have all the evidence we need before our eyes that often productivity increases can keep pace with demand. What happens if demand falls? Oops! There goes the endless bull market theory.

I think we’ve got a few years left of this commodity bull market, and I’m guessing it’ll end between 2016 and 2018. That’s what I’m guessing today, anyway. Sometimes I think it’ll be 2019. I think I’ve guessed before that it would be between 2014 and 2020. There’s nothing consistent about my guesses. (That actually makes me very similar to most market analysts about anything they cover!) The only consistency I have is that I have believed in the commodity bull run theory since the early 2000s, and have always expected it to end in the latter half of this decade. Whether I’m right or should have just kept my darned mouth shut won’t be known for a few years, which allows me a chance to run away and hide if I’ve been wrong. And you’ll forget by then anyway, won’t you?

But it’s good to keep in mind that there are valid reasons to believe the good times might not last forever, even while all around us we’re being given compelling reasons to believe this is a long, long, long gravy train that we’re going to be riding.

Now, speaking of Thomas Malthus, the fine fellow I referred to above, Neil Reynolds of the Globe and Mail wrote a rather excellent piece yesterday in which he discusses the failure of Malthusian thinking when it commodities, and discusses the failure of various “peak” theories to actually work. Remember “Peak Oil?” Hasn’t quite worked out. Reynolds doesn’t have much new to say, but he sums up the situation rather well. Very applicable to the point I was trying to make above, and well worth you reading. So go read it. It’s at: http://www.theglobeandmail.com/report-on-business/commentary/neil-reynolds/our-worlds-not-coasting-on-empty-after-all/article2416024/

Now, I’m gonna re-read that Barclays report and figure out what it means for prairie farmers.