The Chinese hog sector’s rebuild from the Asian swine fever disaster has hastened the government’s policy to end backyard production in favour of large commercial operations.

That also means an accelerated shift away from pigs eating table scraps and swill toward commercial diets.

And that might mean China will have to import more feed ingredients such as soybeans, corn, distillers dried grain, sorghum and peas in the coming years.

But other forces are also at work that could cause the demand to be less than what appears at first glance.

Read Also

Critical growing season is ahead for soybeans

What the weather turns out to be in the United States is going to have a significant impact on Canadian producers’ prices

For example, until the last year or two the portion of China’s hog herd raised in large modern units were fed a formula that had a higher soy meal content than common in the United States and Europe.

Feed makers have started to reduce the ratio of soy meal and increase ingredients such as distillers dried grains, sorghum and synthetic amino acids.

So maybe a greater portion of the herd would eat commercial feed, but the soybean meal inclusion rate would drop.

Also, while Beijing’s goal is to rapidly get back to near self-sufficiency in pork production, it also would like its people to eat less meat.

It has a campaign to encourage reduced meat consumption and another program to cut food waste.

But it is too soon to know if they are having an impact.

And even if China’s middle and upper classes skip a pork meal occasionally, there are still hundreds of millions of people steadily climbing the economic ladder toward a middle class lifestyle that allows them to buy a few more meaty meals.

Clearly there is a lot at play here; forecasting is difficult. But it is undeniable that rapid shifts are occurring.

ASF was devastating for China’s hog producers, but the government and industry have shown fierce determination to recover, to “build back better” to use the catchphrase of the day.

The desire to move away from back yard pen production goes back several years before the ASF outbreak. It was part of the government’s 2016-20 five-year plan.

Authorities wanted an industry with better biosecurity and environmental treatment facilities.

Authorities also believed large, standardized hog operations will have more stable production that leads to reduced price volatility.

Big corporations are the big beneficiaries of the shift to modern production methods and the effort to rebuild production capacity following ASF.

These companies saw their share prices jump higher while investors expected profits would surge as the companies consolidated the industry, rebuilt pig production and sold the pork at very high market prices lingering from the shortages caused by the herd culling.

The poster child of the new, post-ASF situation in China might be Muyuan Foods, the country’s largest swine company, which produced 10 million pigs in 2019.

This year it announced a massive expansion plan valued at $7.8 billion, and among its projects now under construction is a mega farm near Nanyang, Henan, in southwestern China.

Reuters reports that the facility, likely the largest in the world, will eventually house 84,000 sows and their offspring.

It aims to produce 2.1 million pigs a year at that farm alone.

By comparison, Saskatchewan marketed 2.3 million pigs in 2019 and Manitoba marketed 7.8 million.

I wonder if the shift to such gigantic operations will deliver the desired biosecurity and environmental improvements or will they generate their own problems?

Only time will tell.

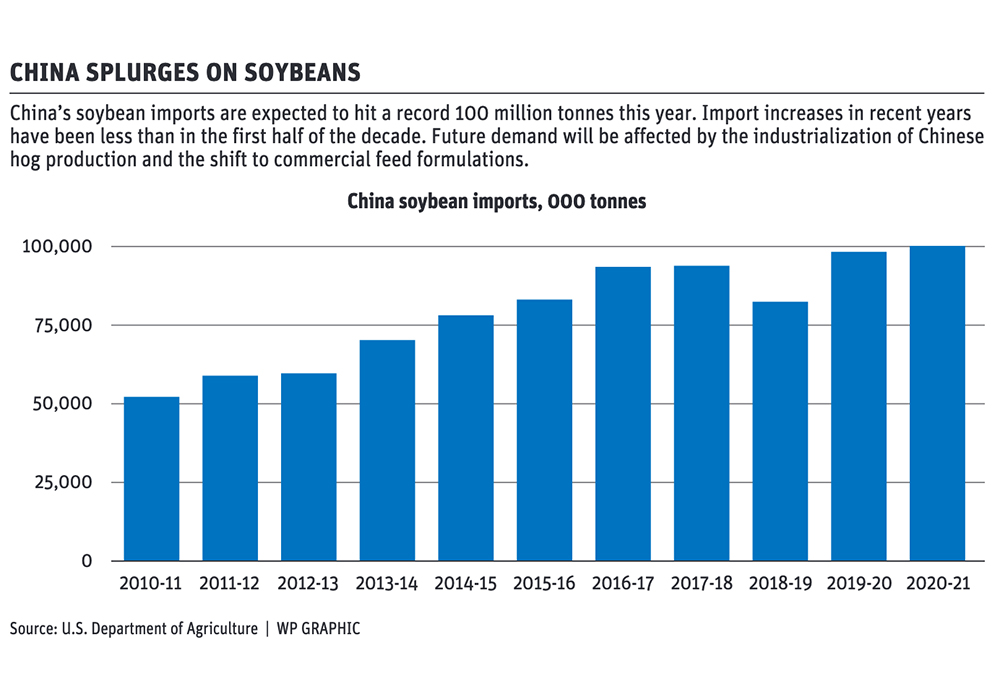

This shift to the corporatization of hog production coincides with a soybean import milestone of 100 million tonnes in 2020, according to a forecast by the United States Department of Agriculture. That is up from 98.5 million the year before.

China’s imports in 2018-19 were severely disrupted by the start of the trade war with the U.S. and it brought in only 82.5 million tonnes that year.

But aside from that anomaly, the 2016-20 period was notable for slower growth in China’s soybean imports, with a cumulative gain of only 6.5 million tonnes over the four years.

In the first half of that decade, gains of five to 10 million tonnes per year were common.

Could we move back to that level of rising soybean demand? Or will the demand be for corn and other feedgrains? Or will it be both?

Again, only time will tell.