SASKATOON — The global urea market is expected to tighten up in the coming years, according to a leading manufacturer of the product.

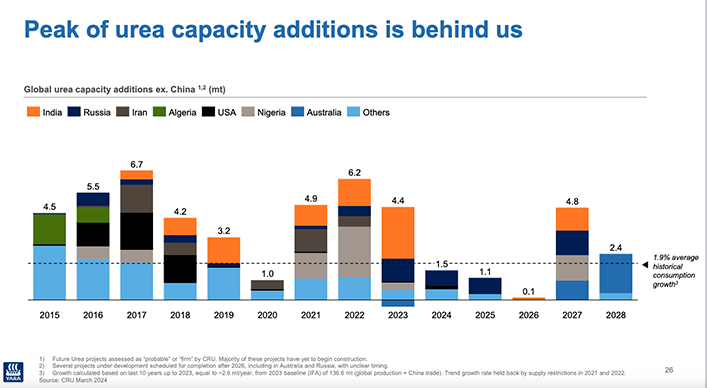

The peak of new capacity additions has passed and there is significantly lower supply growth from 2024 onward.

Related stories:

“This clearly indicates a tightening supply-demand balance longer term,” Yara International chief financial officer Thor Giaever said during a webinar on the company’s first quarter 2024 financial results.

Read Also

VIDEO: Catch up with the Western Producer Markets Desk

The Western Producer Markets Desk provides daily updates on agricultural markets, with recent video commentary including looks into canola, wheat, cattle and feed grains.

It is forecasting 1.5 million tonnes of additional global urea capacity (excluding China) this year, 1.1 million tonnes in 2025 and 100,000 tonnes in 2026.

“The pipeline is historically low,” said Giaever.

It compares to 4.9 million tonnes of additional capacity in 2021, 6.2 million tonnes in 2022 and 4.4 million tonnes in 2023.

Supplies are expected to rebound in 2027 when 4.8 million tonnes of capacity come online, followed by 2.4 million tonnes in 2028.

However, Giaever said that capacity is “highly uncertain” because construction has not yet begun on most of those projects.

Meanwhile, consumption is expected to continue to grow at 1.9 percent per year, which amounts to about two million tonnes per year.

StoneX fertilizer analyst Josh Linville agrees with Yara’s analysis that supplies could be tight over the next three years.

“I don’t think that they are wrong,” he said.

Fertilizer manufacturers are reluctant to build new production facilities because it is an “intense financial commitment.”

“You’re talking billions of U.S. dollars to build these facilities and a very long build time,” he said.

There is also a disincentive to build because producing more product means receiving lower prices for the commodity.

And it is hard to find a place willing to accept such projects these days due to environmental concerns.

Linville agrees that demand growth is going to outstrip supply growth, which means rising prices.

Today’s barge price for urea in New Orleans is about US$275 to $300 per tonne.

“The numbers we’re getting into, I think, are actually kind of attractive,” he said.

It is above the lows of the summer of 2020 when prices were in the upper $100 range, but well below the highs of the spring of 2022 when prices topped $900.

“We are definitely getting back to what could be considered normal,” said Linville.

Tightening global supplies mean prices will rise, but he is not expecting anything “obscene” like what happened in the past few years.

However, if there are supply hiccups caused by rising natural gas prices, further geopolitical turmoil or other factors, the price response could be volatile.

Linville said many growers can’t do much with this information because the product doesn’t deal well with humidity, making on-farm storage tricky.

“Nobody wants to run the chance that they’re going to bring that stuff in, and it’s just going to become a wet pile,” he said.

That is why many farmers do not take advantage of the summer seasonal lows in urea pricing.

Linville said it is possible that some new fertilizer technology could be introduced that fundamentally changes the demand picture.

For instance, India is pushing nanotechnology urea, which it believes could be a game changer that makes the country self-sufficient in urea production.

“It’s something to watch, but we are not willing to change our supply and demand until we actually see that it works and is proven in the field,” he said.

Contact sean.pratt@producer.com