Before I get into the U.S. Department of Agriculture’s crop production report, I’ll mention that the cattle market is beginning to recover.

Fed cattle prices hit the year’s low two weeks ago, an unusual situation because prices usually rise in spring.

However, prices bounced back sharply last week and could continue to rise, although it is not certain they will regain the highs of January.

Carcass weights are falling quickly as the slaughter mix seasonally transitions from yearlings to calves and as beef demand and prices increase going into the prime outdoor grilling season.

Read Also

Pakistan reopens its doors to Canadian canola

Pakistan reopens its doors to Canadian canola after a three-year hiatus.

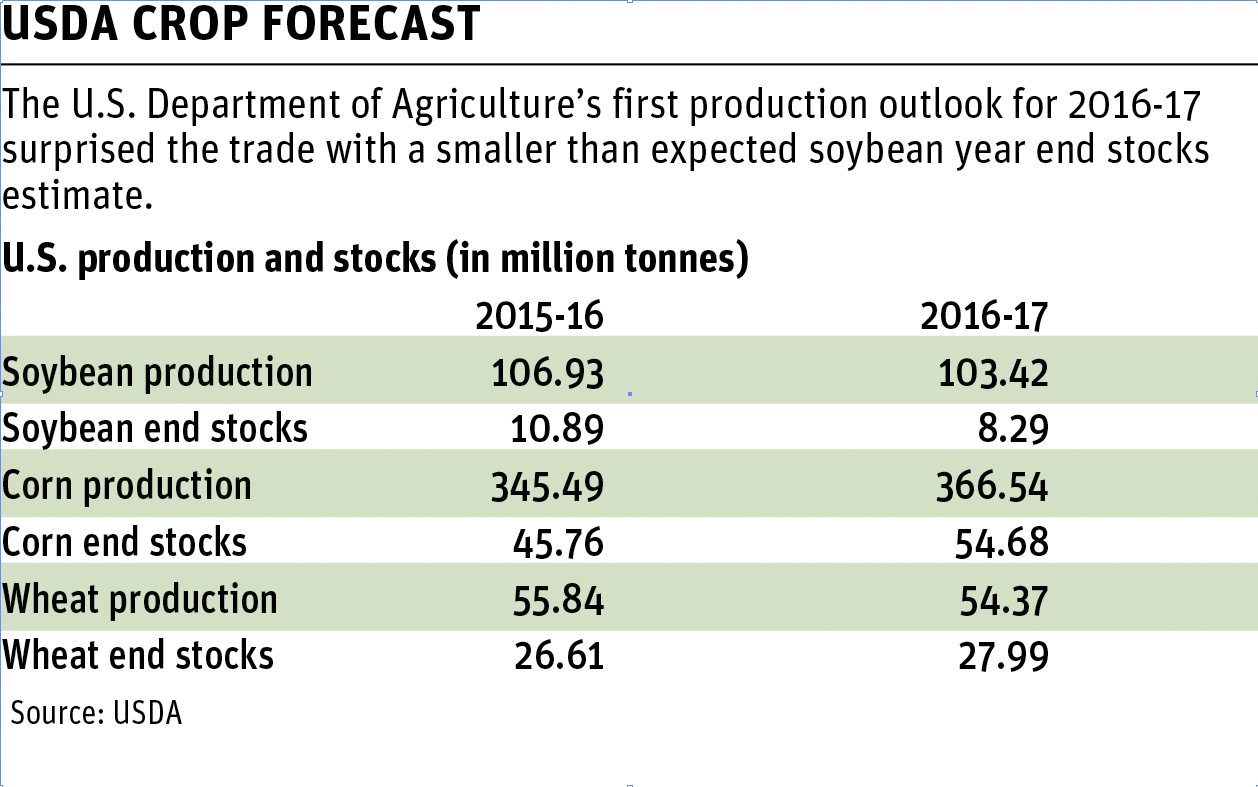

Turning to crops, the USDA surprised the market last week when it forecast smaller than expected soybean production in its first estimates of 2016-17 production.

It sees 2016-17 soybean ending stocks falling to 305 million bushels, or 8.29 million tonnes. The trade had expected 100 million bushels more, or a total of 11 million tonnes.

Its forecasts for corn were mostly neutral.

The stocks outlook for wheat, domestic and global, came in larger than expected. The wheat stocks are mostly accumulating in the United States and China.

Stocks held by Canada, Australia, the European Union, Argentina and Black Sea region are not increasing.

Soybean futures soared almost the daily limit May 10, the day the report was released, which also helped to pull canola higher.

New crop November soybeans jumped as high as US$10.80 a bushel, up 60 cents from where they were trading before the report. The soybean rally also helped lift corn futures.

Soybeans had drifted lower as this column was written May 16 and were trading around $10.55 because the market expects that the soybean rally will cause American producers to switch their seeding plans in mid-campaign and put in more soybeans and less corn.

As I said, the soybean rally also lifted canola futures with new crop November briefly topping $525 May 10, which triggered farmer selling.

The selling and improved moisture conditions in much of Sask-atchewan caused the price to drift lower again.

Alberta and northwestern Sask-atchewan missed the recent rain, but there appear to be good prospects for a series of rainstorms in Alberta beginning late this week and continuing into early next week. Frost last week across the Prairies might cause some reseeding.

The debate over where seeded area will finally wind up will keep crop prices shifting a little, but the biggest factor of course will be the weather.

Crop prospects throughout the Prairies, the U.S. Plains and Midwest, Europe and the Black Sea region look good at this early stage in the season, which is negative for crop prices.

Weather analysts are watching the progression from El Nino to La Nina in the Pacific Ocean because of the potential for the shift to affect North American weather.

Last week’s updates show a rapid cooling of surface water temperatures in the equatorial Pacific.

Several countries’ weather services raised their outlook probability for a La Nina in place by the fall.

However, the big questions are whether it will take hold during the North American summer, and will it be strong enough to increase the potential for warm, dry weather late in the growing season.

The International Research Institute on Climate and Society last week raised the probability of a La Nina taking hold in the June to August period to 52 percent from about 30 percent in the last outlook in mid-April.

The probability rose to 65 percent for the July to September time frame.

Even if La Nina settles in, it is unknown if it would hurt crop production, but it is possible.

If it doesn’t, then expect ample grain supplies from the Northern Hemisphere harvest and a shifting focus to how a La Nina in the September to December time frame affects South American seeding and growing weather.