While the grain market last week devoted most of its attention to the strong pace of United States crop exports, a severe storm in the Midwest and the monthly supply and demand report, wheat watchers wondered if a seasonal low had been reached.

The area around US$5 per bushel has been a level of technical support for Minneapolis hard spring wheat and new crop December futures had fallen near that level early last week as the market focused on new private forecasts from Canada and Russia showing increased production expectations.

Read Also

Volatile temperatures expected for this winter

DTN is forecasting a lot of temperature variability in the Canadian Prairies this winter. Precipitation should be close to average.

But prices did not break below the support and edged higher by the end of the week with support from corn.

This raised speculation that perhaps all the bad news had been priced into the market and the seasonal bottom had been reached.

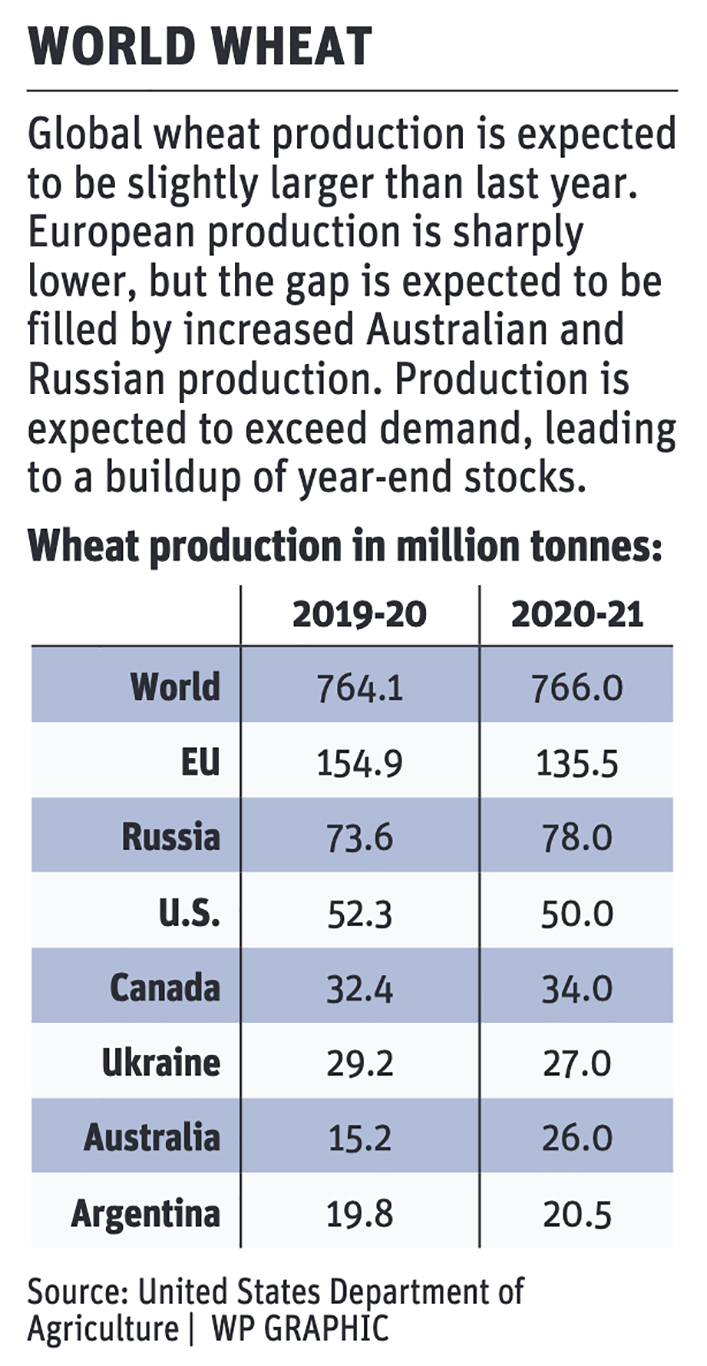

The U.S. Department of Agriculture’s monthly supply and demand report Aug. 11 provided a handy summation of the world wheat situation.

Production in the European Union is expected to fall sharply, but the hole will likely be filled by a strong comeback for Australia’s crop after severe drought last year and also an improved crop in Russia.

The U.S. expects wheat production to be down about two million tonnes from last year, but Canada’s crop is expected to be up about two million, according to the USDA forecast.

Overall, the USDA sees global production to be about the same as last year, outpacing demand for a second consecutive year resulting in increased year end stocks.

That is not a recipe for a booming wheat market.

The USDA revised down its forecast for the year’s average all-wheat price to US$4.50 per bu., from $4.60 in the July outlook and down from the 2019-20 average of $4.58.

Focusing in on Canada, the FarmLink Marketing Solutions crop tour report last week showed a very optimistic outlook for yield potential.

Based on conditions as of July 31 and assuming good weather into harvest, it forecast the potential of wheat (excluding durum) production of 31.9 million tonnes, breaking the previous high set in 2013-14 of 31.1 million.

FarmLink saw the potential for a durum crop of about 6.9 million tonnes, also a record, beating 2013-14’s 6.5 million.

This implies an all-wheat crop of about 38.8 million tonnes, which if correct would force the USDA to raise its forecast for Canada by 4.8 million tonnes from the current level of 34 million.

FarmLink’s forecast might mark the high point of crop potential because there has been little rain across much of central and western Saskatchewan and southern Alberta in the past 30 days.

The heat wave of early August also stressed crops.

However, there is still a good likelihood of great cereal production averages for Western Canada.

To move the production will require another year of strong exports and good rail movement.

Grain movement was great in the second half of the crop year that just ended, as the economic slowdown caused by COVID-19 freed up rail system capacity.

There was a slow start, but by the end of the year, bulk wheat exports topped 18 million tonnes, only 200,000 tonnes behind the previous year.

Bulk durum exports by the end of the year totalled 5.27 million tonnes, which might be a record high for the grain. Strong durum movements to Italy and Turkey were noted.

The direction of wheat prices in the coming few months will, of course, be linked to what happens at harvest but also corn prices could have an impact.

Alas, the corn market is weighed down.

The USDA forecast an enormous, record-breaking 15.3 billion bu. corn crop, up 12 percent over last year.

That was before a storm with hurricane speed winds, called a derecho, hit the Midwest Aug. 9, affecting 37.7 million acres, 14 million of them in Iowa.

Damage is still being assessed, but the market posted only a modest rally from multi-week lows caused by the prospect for a huge crop.

Traders seem to think that storm damage is often overhyped.

The market is also keeping a close eye on weekly corn exports. Given the expected record crop, exceptional exports will be needed to avoid a massive increase in year-end stocks.

Hopes rest on China living up to its trade agreement with the U.S. It didn’t buy much in the first of this calendar year but new crop sales have jumped higher in recent weeks, causing a bit of optimism.

The export sales on the books for new crop corn are indeed good for this time of year but pale compared to the size of the crop and are not as impressive as new crop soybean sales.

The pace of weekly sales would have to be exceptional for many more weeks to raise any real excitement in the corn market.