China’s canola tariffs are obviously front and centre in farmer’s minds at the moment, but global vegetable oil stocks are forecast to tighten in the 2025-26 crop year.

This should bode well for canola demand over the next crop year as the market adjusts to the change in trade flows for Canadian canola.

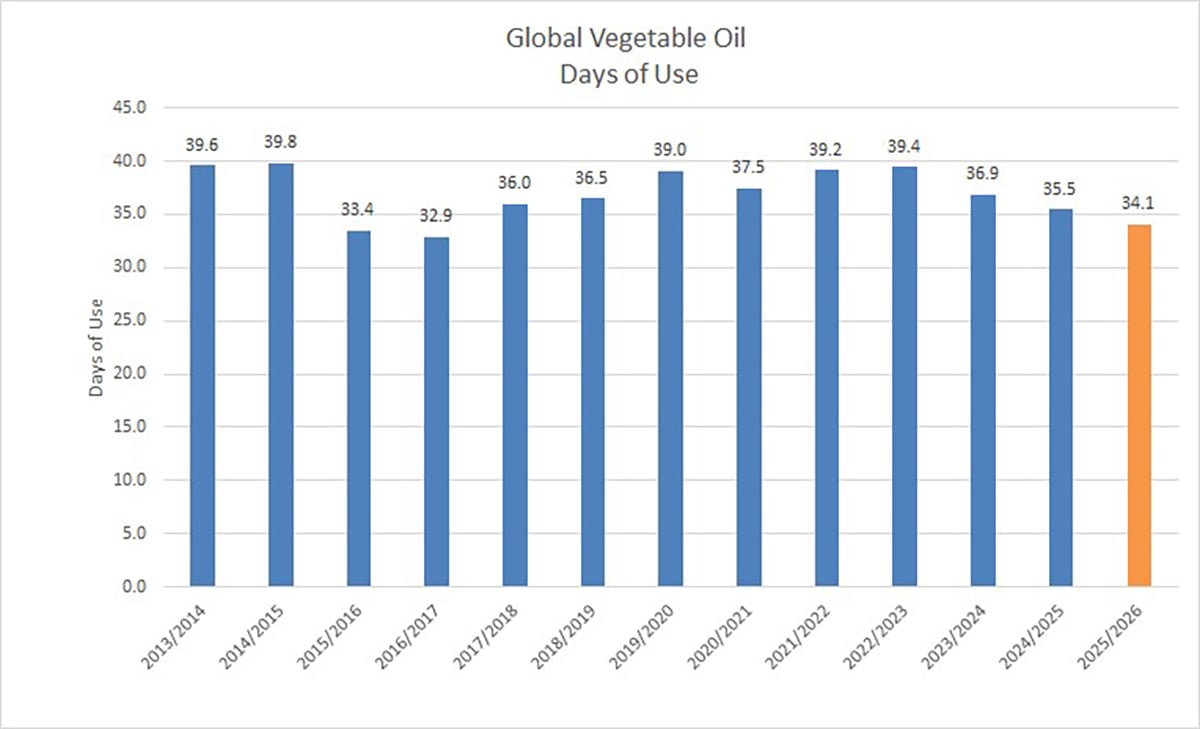

The nine major vegetable oils are expected to drop by 538,000 tonnes to 29.6 million tonnes. This would be the smallest ending stocks level since the 2018-19 crop year. Global canola oil stocks are expected to decline by 218,000 tonnes.

Read Also

VIDEO: Ag in Motion documentary launches second season

The second season of the the Western Producer’s documentary series about Ag in Motion launched Oct. 8.

At the same time, the total demand for vegetable oil is expected to expand by 6.6 million tonnes to 316,509 tonnes in the 2025-26 crop year.

Total vegetable oil demand has increased by 10.3 million tonnes over the past two years. The reason that vegetable oil prices have been strong is that demand is outstripping supply.

Rapeseed (canola) oil demand is also rising, with the U.S. Department of Agriculture forecasting a jump in total demand of 675,000 tonnes to 41.8 million tonnes.

If this demand forecast is accurate, it would be a new record for global rapeseed demand.

Global rapeseed (canola) production is forecast to reach 89.6 million tonnes, which is up by four million tonnes from last year’s output.

The production estimate for 2025-26 is still slightly below the record output of 90 million tonnes in 2023-24. Global rapeseed output is stagnating around the 89 million tonne level.

This provides a positive backdrop for canola demand this crop year. Increased demand combined with flat production will keep rapeseed ending stocks below 10 million tonnes this year.

Although China will not be buying Canadian canola until tariffs are dropped, there is plenty of demand around the globe for canola.