Now and then, it’s a good idea to review the market scenery to check for unusual and extreme price relationships.

There are times when certain markets become cheap while others become expensive. Eventually, these extreme market positions almost always swing to the opposite direction.

Today, we see several outstanding relationships.

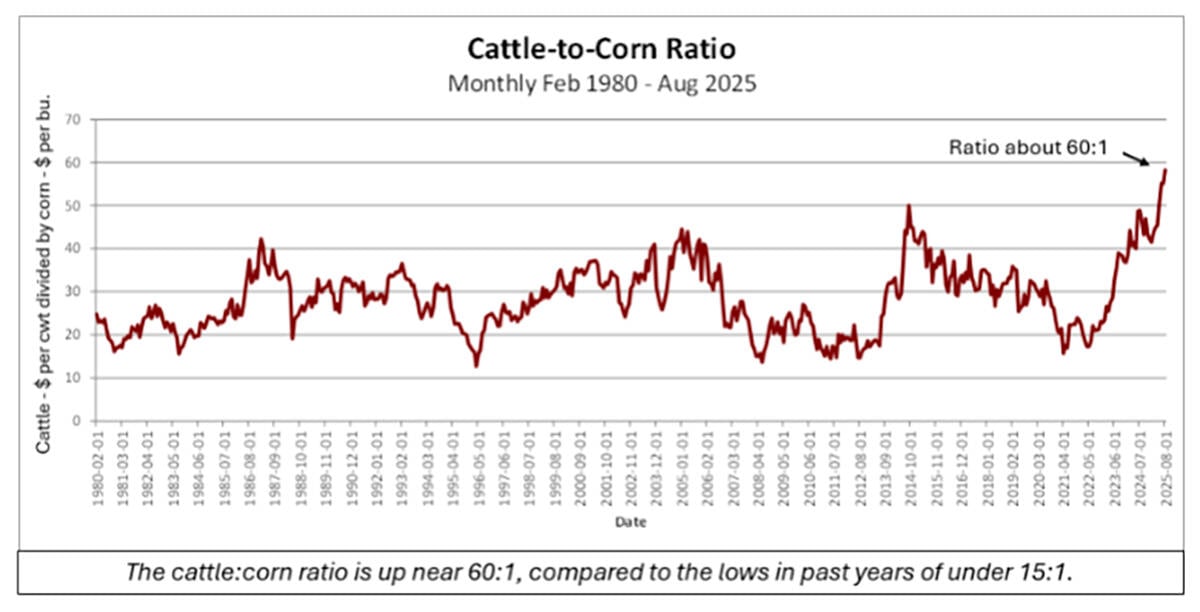

Cattle and corn

Read Also

Flax sector sees omega-3 opportunity

SASKATOON — A global shortage of omega-3 oils could be an opportunity for the flax sector, says an industry official….

The cattle market is flying high. In contrast, corn, a primary ingredient in the production of cattle, is relatively low priced. Never in history have cattle prices been so high relative to corn.

The nearby cattle futures contract recently nosed above US$240/cwt. Not long ago, in 2016, 2019 and 2020, the market was languishing below $100.

On the flip side, nearby corn futures recently dipped below US$3.70/bu., down sharply from the lofty 2022 peak of more than $8.25.

This bull market in cattle has been decades in the making. For years, ranchers and cow-calf operators worked hard for slim returns. There were no incentives for herd expansion. High costs of labour, pastureland and feed caused cutbacks. While other types of farming saw good times, the cattle business remained little changed. A generational shift saw farmers move out of cow-calf operations into more-industrialized pork and poultry businesses and/or cropping. Drought in the vast U.S. and Canadian rangelands didn’t help.

It normally takes several years for high calf and feeder-cattle prices to motivate producers to expand their herds, thereby boosting calf production and beef supply. The cattle bull market and lower grain prices will work to make this happen, but slowly.

Meanwhile, the spread of cattle over hogs — and beef over pork — is extremely wide. High beef prices will eventually curb beef demand, causing the spread to narrow.

That’s what’s new: record-high cattle markets in comparison to other ag markets.

What’s not new

As always, the markets will work to cause a shift. Someday, the spread of cattle over corn will narrow. It’s something for producers to understand, watch for and prepare for in advance. Sooner or (more likely) later, the natural functioning of economics will make it happen.

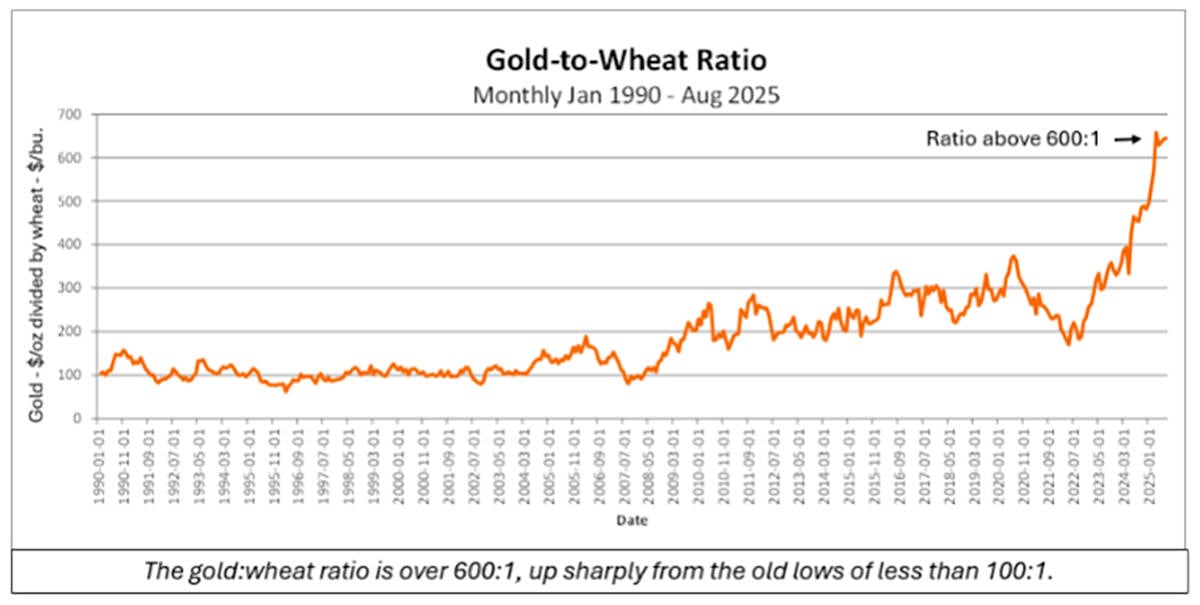

Gold versus grain

Along with cattle, gold is a shining star in the commodity cosmos.

Gold is up by almost 100 times its price in the early 1970s. In 2013 through 2018, gold traded frequently under US$1200 per ounce. Now it’s hovering around $3,400.

Gold is considered to be a currency more than an actual commodity. Some gold is used for industrial purposes. However, more frequently, it’s held as a store of value by individuals, institutional investors and central banks. It is seen as an inflation hedge.

There’s skepticism about the inherent value of conventional currencies produced by, and backed by, governments. Devaluations of various global currencies have been occurring for decades. This is a driver of gold prices. It might mean we’ll see a long-lasting upshift, with gold maintaining a unique status.

Regardless of whether it is sustainable, the ratio of gold over grain has never been wider. From 1990 through 2007, you could buy an ounce of gold with about 100 bushels of wheat. Now it takes more than 600 bushels.

Clearly, grain is in a cheap category while gold is in an expensive one. There may come a time when a lot of people decide it makes more sense to own grain than gold. You can’t eat gold.

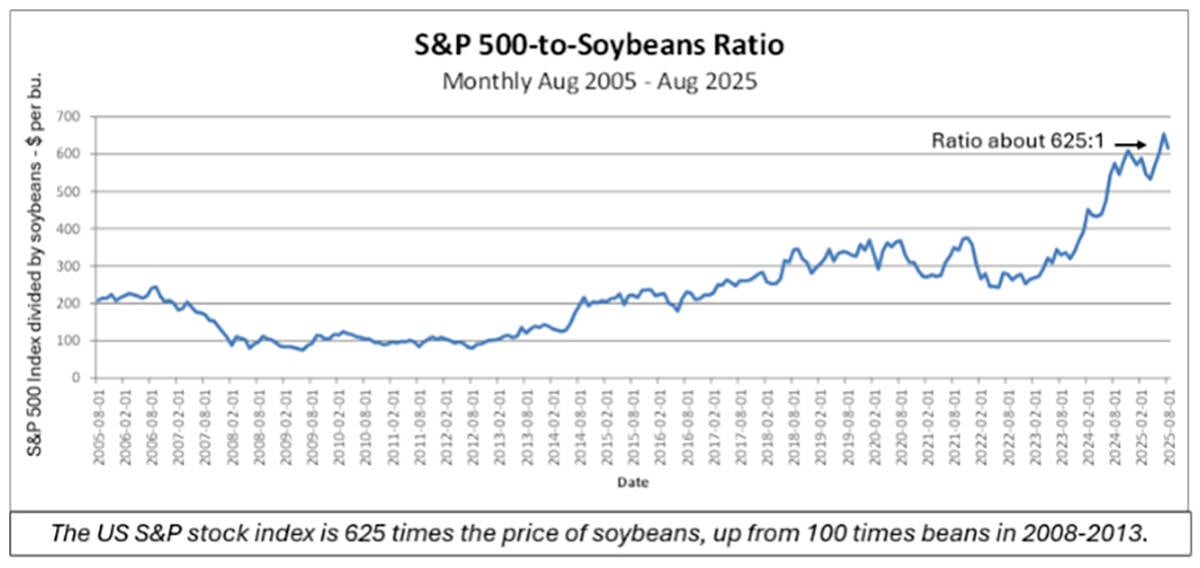

Stocks versus crops

Gold is just one widely owned investment that’s flying high. The major stock indexes have also reached all-time-high territory.

Stocks for some business sectors in the S&P index are so high that savvy investors are having difficulty finding low-priced, low-risk bargains. This is happening while crop futures are down far from their peaks of a few years ago. Looking at the US S&P compared to soybeans (an example from the crop sector), the difference is clear.

There’s no direct correlation between stocks and crops. Even so, someday, stock investors may notice how downtrodden the crop markets are. They might want to get in on the bargains. A few might buy futures. Some may get into crop-related ETFs. Their buying alone might not lift prices significantly, but it won’t hurt either.

Someday too, the farmer with full bins and fields of crops may have a position with less downside risk and more upside potential than the person loaded up with a portfolio of stocks.

There’s more

Checking around, here are some other market relationships to keep an eye on:

- In much of Canada, farmland is high priced relative to crops. Land might stay high. A wide variety of factors account for its pricing. However, with weaker crop prices, at least one supportive factor has been pulled away, if only temporarily.

- Soybean meal looks cheap versus soybean oil. Oil is in the middle of its 15-year trading range. Meal is on the low side of its 15-year range. Meal popped up in mid August, showing signs of life. This has implications for meal users who have benefitted from the low cost of this protein feed the past year.

- Natural gas has traded quietly, in a low-level range, for almost three years, an oddity in an environment of otherwise volatile markets. Users of natural gas are the beneficiaries of the low prices. But for how long?

- The cost of your morning coffee is going up. That’s partly because global coffee prices have exploded. There’s not much you can do about it — except keep drinking it to stay sharp and alert — recognizing that, when a commodity gets misaligned, you will eventually see a correction.