Feedlots are expected to bid up the price of feeder cattle so that margins in the deferred positions cover variable costs

Glacier FarmMedia – For the week ending Jan. 11, western Canadian feeder cattle prices were up $15-$20 per hundredweight compared to the week ending Dec. 21.

In eastern Saskatchewan and Manitoba, quality packages of steers 800 pounds and heavier traded $20-$25 per cwt. higher compared to three weeks earlier.

Alberta packers were buying fed cattle on a dressed basis in the range of $432-$438 per cwt. delivered this past week, up from the average level of $420 per cwt. on Dec. 19.

Read Also

Short rapeseed crop may put China in a bind

Industry thinks China’s rapeseed crop is way smaller than the official government estimate. The country’s canola imports will also be down, so there will be a lot of unmet demand.

U.S. packers were buying fed cattle on a live basis around $270 per cwt. f.o.b. feedlot in southern Alberta, up $8-$10 per cwt. from three weeks earlier.

Strength in the live cattle cash and futures markets contributed to the surge in the feeder complex. The April live cattle futures are testing the psychological $200 level, which is an historical high. The live and feeder cattle futures are incorporating a risk premium as extreme winter weather blankets Texas, Oklahoma and parts of Nebraska and Kansas.

In central Alberta, Simmental-Angus cross steers weighing slightly less than 900 pounds on barley and silage diet with full processing data sold for $375 per cwt. In the same region, larger-frame, lower-flesh black heifers around 1,015 pounds settled at $318 per cwt.

At the Heartland sale in Yorkton, Sask., tan steers weighing 865 lb. dropped the gavel at the psychological $400 per cwt. level, while their younger brothers weighing 717 lb. silenced the crowd at $448 per cwt.

Near Calgary, larger frame black heifers averaging 840 per cwt. apparently sold for $340.

On the Whitewood, Sask., auction market report, tan steers weighing 705 lb. were valued at $444, and tan heifers averaging 708 lb. were last bid at $387.

In central Alberta, a smaller package of 566-lb. mixed steers sold for $510, and mixed heifers weighing 588 lb. were valued at $431.

Feedlot margins have improved and are in positive territory for the first four months of 2025.

Break-even pen closeouts for January are in the range of $262-$268 for all costs. For February, the break-even fed cattle price is in the range of $260-$265.

The April live cattle futures reached up to $198 on Jan. 9, which would result in an Alberta cash price around $278-$282. For March and April, the Alberta break-even fed cattle price is in the range of $255-$260.

Feedlots will bid up the price of feeder cattle so that margins in the deferred positions cover variable costs, which are feed and interest. This is the upper limit for feeder cattle prices in the short term.

Given the current prices, margins are in negative territory on incoming replacements.

For June and July, the Alberta break-even fed cattle price to cover feed and interest is in the range of $270-$275 per cwt., and feedlots need $292-300 per cwt. to cover variable and fixed costs.

The June live cattle futures have been hovering at $193, and using the current exchange and normal basis, the Alberta fed price would be $272-$275 per cwt. The feeder market has run it’s course for the time being.

The United States has experienced year-over-year declines in the calf crop since 2018. The Canadian calf crop has been shrinking since 2022.

U.S. feeder cattle outside finishing feedlots as of Jan. 1, 2025, are expected to be 23.4 million head. This is down 776,000 head from Jan. 1, 2024, and down 1.8 million head from Jan. 1, 2023.

In Western Canada, feeder cattle outside finishing feedlots as of Jan. 1, 2025, are expected to total 2.81 million head, down 160,000 head from Jan. 1, 2024, and down 246,100 head from Jan. 1, 2023.

At the time of writing this article, talk in the trade was that the U.S. is expected to resume imports of Mexican feeder cattle during the week of Jan. 20. The import pace during the first couple weeks will be slower as the trade works through new procedures and protocols. The industry is expecting imports to increase drastically by the end of February. This will take some of the steam out of the feeder cattle market.

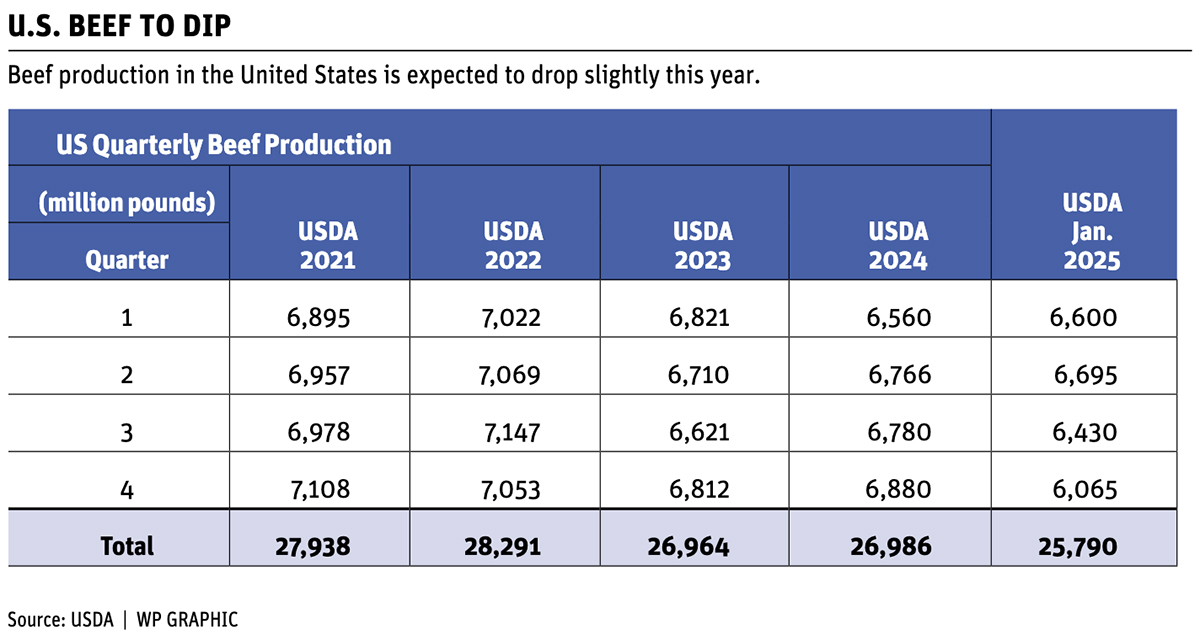

The U.S. Department of Agriculture lowered beef production forecasts for each quarter of 2025. Notice that U.S. third quarter beef production is expected to drop to 6.430 billion lb., down 350 million lb. from the third quarter of 2024. U.S. fourth quarter production is expected to fall to 6.065 billion lb., down 815 million lb. from the fourth quarter of 2024.

Lower production in the latter half of 2025 is driving the calf price higher. It’s not logical that U.S. president-elect Donald Trump would tariff cattle or beef, given the country’s tighter supplies.

Barley prices are expected to trend higher. Statistics Canada’s November crop survey had the 2024 barley crop at 8.144 million tonnes, down from the 2023 output of 8.905 million tonnes and down from the 10-year average of 9.4 million tonnes.

Supplies are down from year-ago levels, while barley exports and domestic use are higher than year-ago levels. Statistics Canada will release its Dec. 31 Stocks Report on Feb. 7. Canadian on-farm barley stocks as of Dec. 31 are expected to come in at 4.7 million tonnes, down from the Dec. 31, 2023, on-farm stocks of five million tonnes.

The feed barley market has potential to jump $30-$40 per tonne later in spring, which would temper the upside for the feeder cattle market. The barley market needs to trade at a premium to U.S. corn so that more feedlots switch over to corn in the rations.

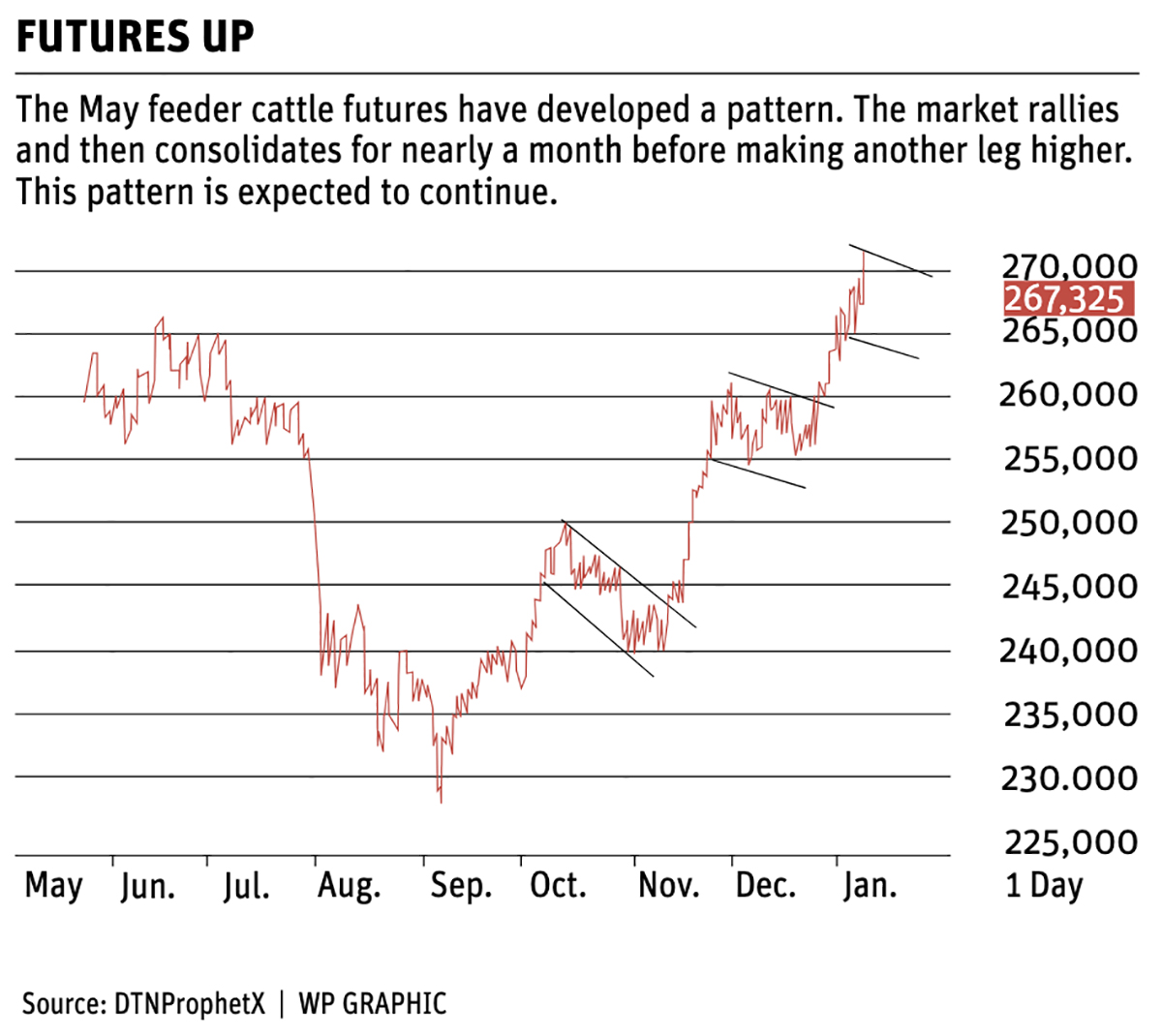

The May feeder cattle futures have developed a pattern. The market rallies and then consolidates for nearly a month before making another leg higher. This pattern is expected to continue.

Look for the market to consolidate during January and then rally up to the range of $280-$285 in February. The managed money had a net long of 20,344 contracts on Dec. 31, which was the largest long in the past couple of years.

In conclusion, the cash feeder market has likely run it’s course in the short term because margins in the finishing sector barely cover variable costs for the summer.

The U.S. will resume imports of Mexican feeder cattle later in January.

The futures market is due for a consolidation period because the funds are out of buying power.

Longer term, we’re expecting the feeder market to percolate higher as lower feeder cattle supplies result in a sharp year-over-year decline in beef production during the final quarter of 2025.

Jerry Klassen is the president and founder of Resilient Capital, specializing in proprietary commodity futures trading and market analysis. He can be reached at 204-504-8339 or via his website at resilcapital.com.