For the week ending March 14, western Canadian feeder cattle markets traded $10-$15 per hundredweight higher than seven days earlier.

Feeder cattle prices recovered from the U.S. tariff-related weakness that occurred from March 4-6. Finishing feedlots were aggressive across all weight categories.

Many operations moved a portion of their cattle to custom feedlots in the United States to avoid the tariffs. This may have contributed to the higher risk tolerance now that the tariffs have been removed until April 2.

Read Also

Short rapeseed crop may put China in a bind

Industry thinks China’s rapeseed crop is way smaller than the official government estimate. The country’s canola imports will also be down, so there will be a lot of unmet demand.

There was limited slippage on fleshier replacements. Grassers were once again trading at or near record highs with ideas that yearling numbers will be down sharply come August.

In central Alberta, black Simmental cross heifers weighing slightly more than 800 pounds on a backgrounding diet with full health data sold for $359. In the same region, a smaller package of larger frame thin mixed steers weighing 805 lb. reportedly traded for $398.

Southeast of Calgary, a smaller package of larger frame mixed heifers evaluated at 703 lb. reportedly dropped the gavel at $395. In the same region, larger frame Angus cross steers with lighter flesh levels with a mean weight of 710 lb. reportedly sold for $440.

South of Edmonton, larger frame black steers weighing 555 lb. moved through the ring at $530. Prices were basically back up near historical highs, especially on the lighter weight categories.

Alberta plants were buying fed cattle on a dressed basis in the range of $450-$460 per cwt. delivered, up from the previous week’s values of $430-$450 per cwt. Using a 60 per cent grading, this equates to a live price of $270-$276 per cwt.

Break-even pen closeouts for March are in the range of $255-$260 per cwt. The healthy feeding margins are the main factor supporting the feeder complex.

Market-ready fed cattle supplies in Alberta and Saskatchewan on April 1 are expected to drop to 81,000, down about 12,000 head from last year. This is a seasonal low.

If the U.S. tariffs are once again paused in April, the Alberta fed market will need to ration demand by trading at a premium to U.S. values.

Fed cattle supplies will be extremely tight until mid-May. Feeding margins have potential to improve over the next 30 to 45 days, which could lift the feeder market $5-$10 per cwt. higher.

Market-ready fed cattle supplies in Alberta and Saskatchewan during May will increase to 150,000 head. This will be followed by a seasonal high of 280,000 head in June.

Even under a normal environment, the Alberta fed cattle market is expected to trend lower from mid-May though June and July. This will result in softer feeder prices during the late spring and early summer period.

Feed barley and U.S. corn offers in southern Alberta have dropped $10-$15 per tonne over the past couple of weeks.

The Lethbridge barley market was quoted at $295-$305 per tonne delivered, while central Alberta operations were showing bids from $280-$295 per tonne.

U.S. corn was offered in the range of $325-$330 per tonne delivered in southern Alberta. Farmers have stepped up sales over the past week while larger operations have the bulk of their requirements covered for March, April and May.

Canadian farmers are expected to seed 6.280 million acres of barley this spring, according to Statistics Canada. This was down two per cent from last year. The acreage survey was conducted from Dec. 13, 2024, to Jan. 17, 2025.

Needless to say, this was before the Chinese tariffs on canola oil and meal and the major Trump threat.

We are expecting Canadian farmers to seed 6.9 million acres of barley this spring, which would be up eight per cent, or 512,000 acres, from last year.

U.S. farmers are expected to seed 94 million acres of corn this year, according to the U.S. Department of Agriculture. This would be up 3.7 per cent, or 3.4 million acres, from last year. Barring adverse weather, feedgrain supplies will be abundant during the fall period, which will be supportive to the feeder cattle market.

For the week ending March 1, Canadian feeder cattle exports to the U.S. were 33,025 head, up 12,427 head from last year for the same period.

The year-over-year increase reflects the number of Canadian-owned cattle shipped to the U.S. before March 4 due to the tariff threat. This doesn’t necessarily reflect stronger U.S. demand for Canadian feeders.

In the U.S., imports of Mexican feeder cattle are running below expectations, which is supportive for the U.S. feeder market.

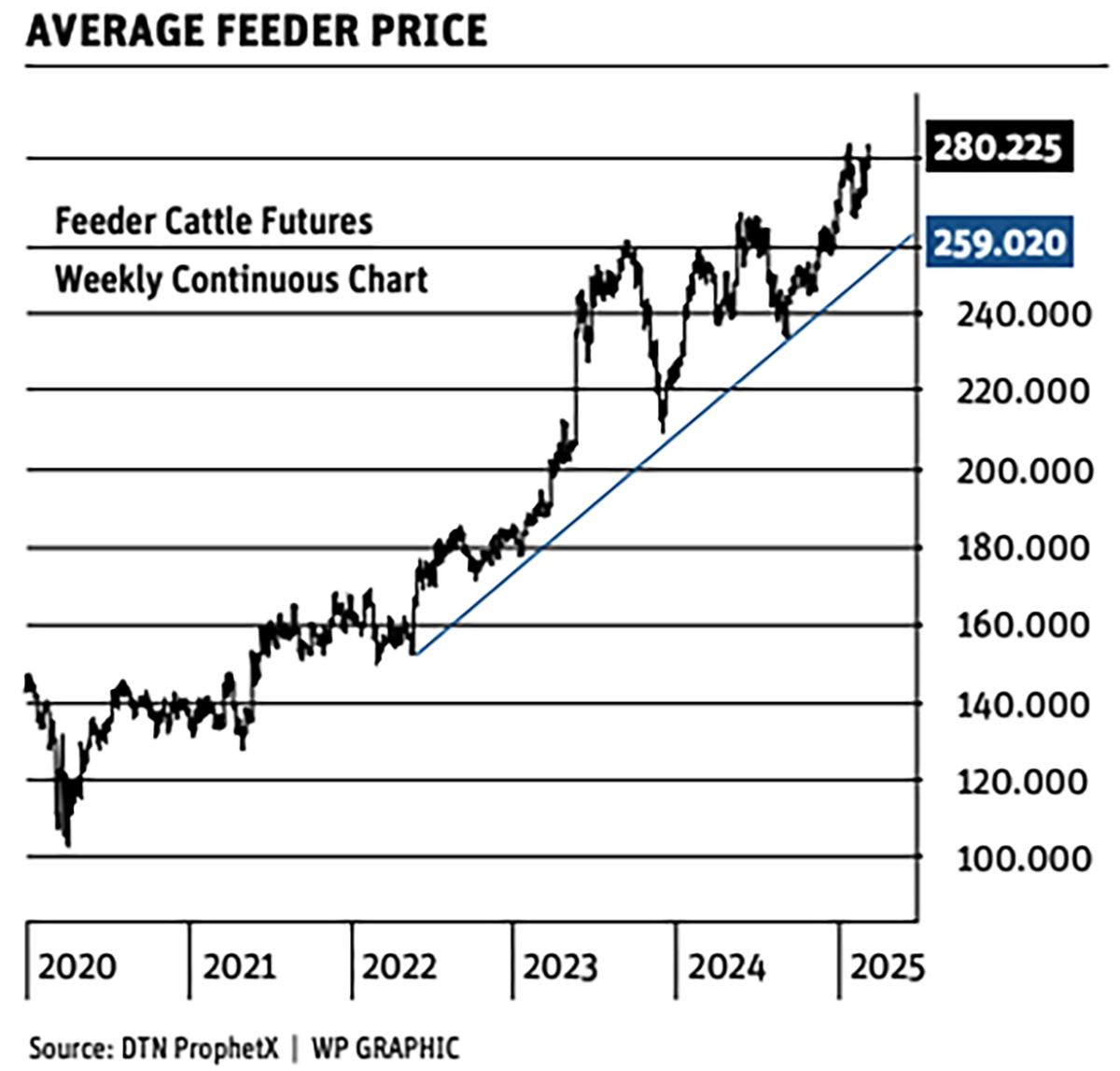

The feeder cattle futures market continues to trend higher. For the week ending March 4, the managed money was a net buyer of 611 contracts while the commercial was a net seller of 33 contracts.

Managed money buying and commercial selling characterize a bullish or upward trending market.

As of March 14, the managed money long is estimated at 30,000 contracts, which is record long.

The futures market will likely turn in May. Beware because the funds will all want to liquidate at the same time. The large fund position and the looming tariff threat encourages cow/calf and backgrounding operators to get their price insurance as soon as possible.

The CME composite price is the official cash settlement price for the CME feeder cattle futures at contract final settlement. Figures have been calculated by the CME Group from prices reported by the USDA. Below is the seven-day average price for 700-899-pound feeder steers.

- March 4 — $277.87

- March 5 — $276.09

- March 6 — $273.77

- March 7 — $273.95

- March 10 — $276.54

- March 11 — $278.71

U.S. beef demand has potential to significantly decline in the summer months and result in softer U.S. fed and feeder cattle prices.

Under the leadership of president Donald Trump, the U.S. has or will implement tariffs on its four largest trading partners.

Since the COVID low of 2020, the Dow Jones Industrial Average has gone from 20,000 to a high of 45,000, which occurred in November 2024. U.S. corporations have experienced three quarters (nine months) of record profits. After four years of growth, the U.S. economy is entering a contraction phase.

These tariffs could shave 25-30 per cent off the equity markets. The Dow Jones has potential to be trading around 30,000 to 33,00 by the end of 2025.

Walmart Inc., Home Depot Inc. and Target Corp. have all raised concerns about weaker consumer spending, which comprises about two-thirds of U.S. gross domestic product. A one per cent decrease in consumer spending equates to a one percent decrease in beef demand.

The U.S. has experienced historically low unemployment since December 2021. We’re going to see higher U.S. and Canadian unemployment levels later in summer.

This is the signal to make sure you have your price insurance on yearlings that will be sold in August or September. Make sure you have your price insurance on calves that will be sold in the fall.

There tends to be a three to four month lag when between the Dow and the cattle futures when the economy moves into a recession. When the cattle market turns lower, there will be a significant move to the downside.

The market has maintained the upward trend since the COVID lows of 2020. When the market breaks the upward trendline, there will be a significant move to the downside.

Jerry Klassen is president and founder of Resilient Capital, specializing in proprietary commodity futures trading and market analysis. He can be reached at 204-504-8339 or via his website at resilcapital.com.