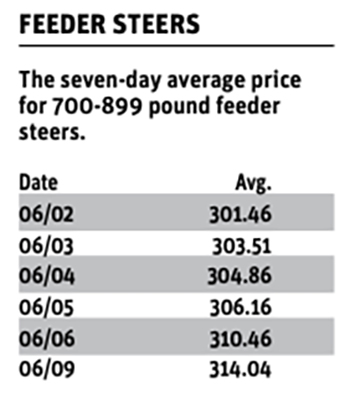

For the week ending June 13, western Canadian feeder cattle markets were relatively unchanged compared to seven days earlier.

The United States closed its border to Mexican feeder cattle on May 11 due to the advancing detection of new world screwworm.

The feeder cattle cash and futures markets appear to be incorporating a risk premium due to the uncertainty in supplies.

Read Also

The Western Producer Livestock Report – October 9, 2025

Western Producer Livestock Report for October 9, 2025. See U.S. & Canadian hog prices, Canadian bison & lamb market data and sales insights.

During April, U.S. imports of Mexican feeder cattle were averaging 20,000 head per week. Ideas are that the U.S. border will open to Mexican feeders later in fall, but the actual date is unknown. This has resulted in lower U.S. beef production estimates for the final quarter of 2025 and first quarter of 2026.

Secondly, the U.S. has tariffs of 10 per cent on Australian, New Zealand and Argentine beef.

Brazilian beef is tariffed at 36.4 per cent, while Nicaraguan beef is tariffed at 18 per cent.

Beef demand is inelastic. In this type of market structure, the U.S. consumer pays the bulk of the tariff. Wholesale beef and retail beef prices have made fresh historical highs over the past month as the tariffs are passed down the chain of demand.

Feedlots are anxious to secure ownership of replacements, given the healthy margin structure.

On June 11, U.S. wholesale Choice beef was valued at US$371 per hundredweight, up $23 per cwt. from a month earlier, while Select product was quoted at $359 per cwt., up $26 per cwt. from average values during the second week of May.

U.S. restaurant traffic continues to run eight to 10 per cent above year-ago levels.

In Canada, daily restaurant traffic has been reported 18 to 30 per cent above last year.

Government and industry data on food spending is contrary to financial results and forward guidance from major chains such as McDonald’s and Wendy’s.

On June 12, Alberta packers were buying fed cattle on a dressed basis at $502-$505 per cwt. delivered, up $10-$12 per cwt. from a month earlier. Live prices in southern Alberta were quoted at $298 per cwt. f.o.b. feedlot, and break-even pen close-out values are around $270 per cwt.

North of Saskatoon, mixed steers on backgrounding ration with full preconditioning averaging 1,000 pounds sold for $390 per cwt. f.o.b. farm.

At the Killarney, Man., sale June 9, a smaller package of black steers with mean weight of 909 lb. dropped the gavel at $432 per cwt. At the same sale, black steers evaluated at 817 lb. reportedly sold for $460 per cwt.

At the Ponoka, Alta., sales June 11, Angus Simmental cross heifers scaled at 841 lb. with full processing data on mostly hay diet were last bid at $421 per cwt.

At the Dawson Creek, B.C., sale, a larger package of 715 lb. Angus steer calves on light grain and hay diet on full herd health program sold for $494 per cwt. At the same sale, a smaller package of mixed heifer calves weighing 700 lb. reportedly moved at $440 per cwt.

At the Westlock, Alta., sale, mixed weaned steers on the card at 625 lb. on silage and hay diet with preconditioning records traded for $548 per cwt.

The Killarney sale report had a smaller package of 600 lb. steers notching the board at $599 per cwt.

At the Dawson Creek sale, Angus-based heifers on light grain and hay diet with full herd health data averaging 633 lb. settled at $485.

In Manitoba, there were reports of Ontario and U.S. orders resulting in a premium over Alberta prices in some cases.

Southeast of Calgary, steer calves of higher quality genetics weighing 500-525 lb. were trading from $608 per cwt. to as high as $628 per cwt.

Cow-calf producers are selling calves for September through November delivery. Values are quoted $20-$30 per cwt. below current levels. Buyers have incorporated a discount in anticipation of the opening of the U.S. border to Mexican feeder cattle.

As well, the June 2026 live cattle futures are trading at a US$22 per cwt. discount to the June 2025 contract.

For yearlings off grass, the market for August and September is trading at a $10-$15 per cwt. discount from prices of similar weight quoted in this issue.

Strength in the fed cattle market has underpinned the nearby feeder cattle prices. Supplies of market-ready fed cattle are not considered tight.

In the U.S., cattle on feed 150 days or longer as of May 1 were 3.316 million head, up 111,000 head from May 1, 2024.

U.S. dressed weights are running 25 lb. above year-ago levels.

In Alberta and Saskatchewan, cattle on feed 150 days or longer on May 1 were 380,376 head, down only 6.7 per cent, or 27,203 head, from May 1, 2024.

Western Canadian steer weights are up six lb. from last year while the heifer average is up 37 lb. from the first week of June 2024.

In addition to building fed cattle supplies, restaurant and grocery store spending dips to seasonal lows in September. We expect to see pressure on the fed cattle market during August and September, which would weigh on the feeder cattle market.

The CME composite price is the official cash settlement price for the CME feeder cattle futures at contract final settlement. Figures have been calculated by the CME Group from prices reported by the U.S. Department of Agriculture.

The Commitments of Traders Report suggests that feeder cattle futures are at or near a top for the time being.

As of June 3, the commercial trader was net short 9,921 contracts, while managed money was net long 33,639 contracts. Both of these net positions are at records.

The speculative money is out of buying power. When the commercial and managed money are at extremes, the market tends to reverse.

There is an old saying among futures traders that the market moves to the level where the most number of people will lose money. In this case, the futures market will move down. Keep in mind the commercial trader is considered the “smart money.”

Drier conditions in Western Canada are a concern for barley production.

At the time of writing this article, a large portion of Saskatchewan and Alberta had received less than 40 percent of normal precipitation over the past 30 days. Timely rains are needed to sustain yield potential.

Production estimates from barley traders are all over the map. The main point is that barley production will be down from last year, and Western Canada will need about two to 2.5 million tonnes of U.S. corn to satisfy feed demand in the 2025-26 crop year.

The longer term forecasts for the western half of the U.S. Midwest calls for below normal precipitation and above normal temperatures. As of June 12, growing conditions have been nearly perfect in the U.S.

A change in weather will cause the corn market to experience a significant rally, which would cause the feeder cattle cash and futures market to drop sharply. The next two months will determine the size of the Canadian barley and U.S. corn crops.

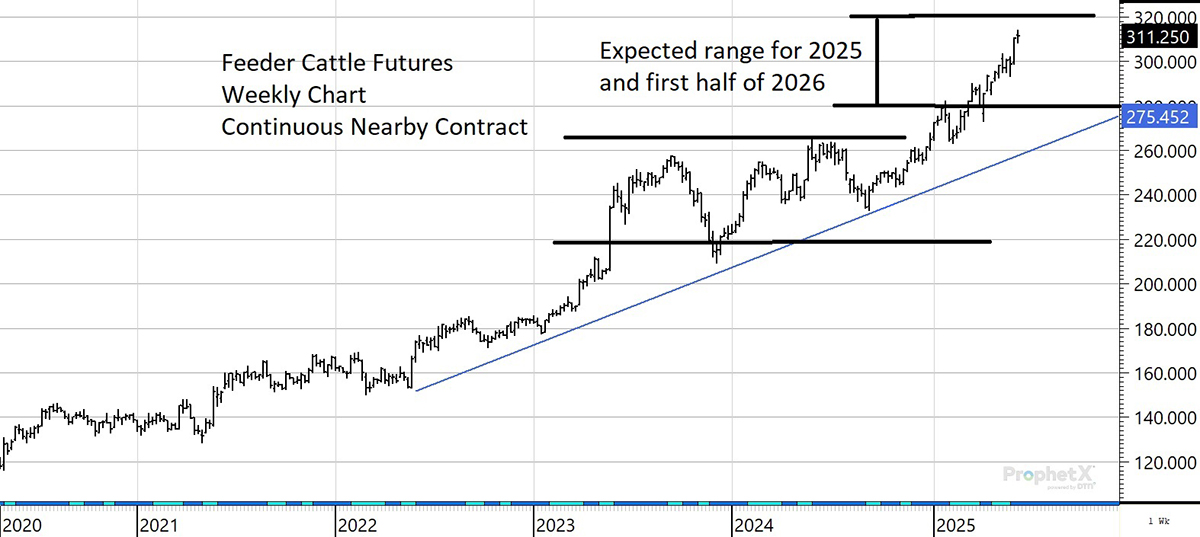

From May 2023 through December 2024, the feeder cattle futures traded in a range with support at $220 and resistance at $260.

After the recent rally, we’re now looking for the market to establish another range for the next 12 to 18 month period. Our ideas are that the market will trade in the range of $280 to $320.